Articles

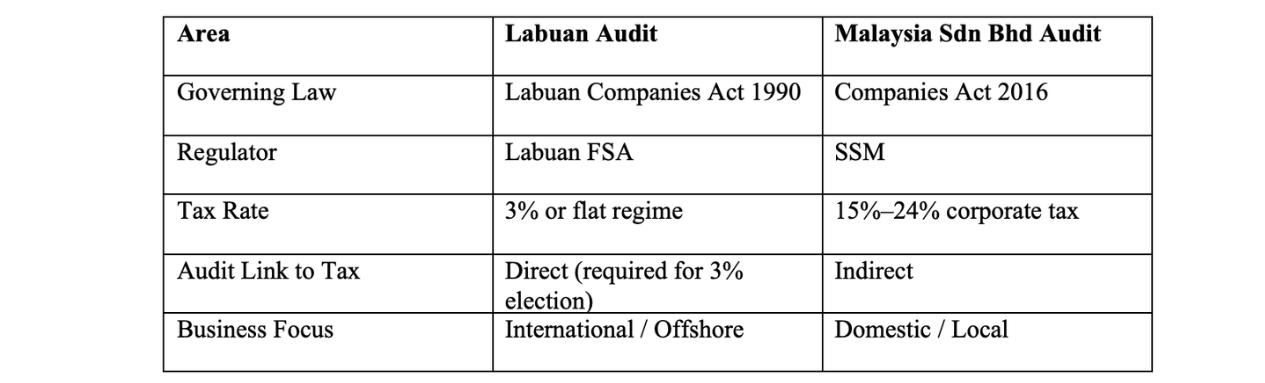

Labuan vs Sdn Bhd: Audit Differences

Do you fall under Labuan audit requirements or Malaysia Sdn Bhd audit obligations?

Although both involve statutory audits, the governing laws, tax treatment, and reporting standards differ significantly. Below is a clear breakdown.

Governing Laws

🏛️ Governing Authority & Regulator

All Labuan entities are regulated by the Labuan Financial Services Authority (Labuan FSA.

📜 Key Applicable Legislation

Depending on your business structure and activities within Labuan IBFC, operations are governed by a robust suite of legislation:

• Corporate Framework: Labuan Companies Act 1990 (governs incorporation, administration, and company structures).

• Specialized Financial Activities: Labuan Financial Services and Securities Act 2010 or Labuan Islamic Financial Services and Securities Act 2010 (for banking, insurance, fund management, and digital assets).

• Alternative Structures: Labuan Trusts Act 1996 or Labuan Foundations Act 2010.

Mainland Malaysia (Sdn Bhd) Framework

🏛️ Governing Authority & Regulator

All mainland private limited companies are regulated by the Companies Commission of Malaysia (Suruhanjaya Syarikat Malaysia - SSM).

📜 Key Applicable Legislation

• Corporate Framework: Companies Act 2016 (governs the entire lifecycle of incorporation, compliance, directorship, and winding up).

Audit Scope Differences

| Audit Focus | Labuan entities | Malaysia Sdn Bhd | |

| Primary Objective | Regulatory Compliance & Tax Gatekeeper | Financial Accuracy & Governance | |

| Tax implication from audit | Verifies eligibility for 3% trading tax or 0% holding tax. | Prepares standard corporate tax data for LHDN (standard 24% or SME rates). | |

| Substance Requirement Check | Must verify minimum local employees and local operating expenses. If SR not met, entity tax at 24% on its net profit. | Not applicable. | |

| Accounting Standard | MFRS or MPERS (domestic standards). | MFRS or MPERS (domestic standards). |

Tax Implication

Under the Labuan Business Activity Tax Act 1990:

- 3% tax on net audited profits (for Labuan trading activities), or

- RM20,000 flat tax (for certain non-trading activities, subject to current rules)

Malaysia Sdn Bhd Tax

Governed by the Income Tax Act 1967:

- Standard corporate tax rate: 24%

- SME rate: 15%–17% on first chargeable income threshold (subject to prevailing rules)

Reporting Standards

Financial statements may be prepared under:

- IFRS

- Malaysian Financial Reporting Standards (MFRS)

- Other approved accounting standards (subject to Labuan FSA requirements)

Malaysia Sdn Bhd

Financial statements must comply with:

- MFRS or MPERS

- Filed with SSM annually

Conclusion

A proper understanding of Labuan audit requirements ensures:

- Tax efficiency

- Regulatory compliance

- Smooth annual filings

- Reduced penalty risks

Latest Insight & Articles

Your Labuan Audit Partner

Trusted Expertise in Labuan Financial Services Compliance

Kuala Lumpur Office

38D, 3rd Floor, Jalan Radin Anum, Bandar Baru Sri Petaling, 57000 Kuala Lumpur, Malaysia

Petaling Jaya Office

D-1-32, Block D, 8 Avenue, Jalan Sungai Jernih 8/1, Section 8, 46050 Petaling Jaya, Selangor Darul Ehsan, Malaysia

Labuan Office

Office Suite 1605, Level 16 (A), Main Office Tower, Financial Park Complex Labuan, Jalan Merdeka, 87000 Labuan F.T, Malaysia